在上一篇文章中,我们讨论了如何使用 python 获取 nifty 和 bank nifty 数据。那篇文章的反响很好,因此根据大众的需求,这里有一个扩展版本。在本文中,我们将学习如何每 30 秒从 nse 网站获取期权链数据。此内容仅用于学习目的。

在 python 中,我们将使用 asyncio 每 30 秒向 nse 数据发出一次 api 请求。

在python中安装所需的库

pip 安装 aiohttp 异步

代码

import aiohttpimport asyncioimport requestsimport jsonimport mathimport timedef strRed(skk): return "�33[91m {}�33[00m".format(skk)def strGreen(skk): return "�33[92m {}�33[00m".format(skk)def strYellow(skk): return "�33[93m {}�33[00m".format(skk)def strLightPurple(skk): return "�33[94m {}�33[00m".format(skk)def strPurple(skk): return "�33[95m {}�33[00m".format(skk)def strCyan(skk): return "�33[96m {}�33[00m".format(skk)def strLightGray(skk): return "�33[97m {}�33[00m".format(skk)def strBlack(skk): return "�33[98m {}�33[00m".format(skk)def strBold(skk): return "�33[1m {}�33[00m".format(skk)def round_nearest(x, num=50): return int(math.ceil(float(x)/num)*num)def nearest_strike_bnf(x): return round_nearest(x, 100)def nearest_strike_nf(x): return round_nearest(x, 50)url_oc = "https://www.nseindia.com/option-chain"url_bnf = 'https://www.nseindia.com/api/option-chain-indices?symbol=BANKNIFTY'url_nf = 'https://www.nseindia.com/api/option-chain-indices?symbol=NIFTY'url_indices = "https://www.nseindia.com/api/allIndices"headers = {'user-agent': 'Mozilla/5.0 (Windows NT 10.0; Win64; x64) AppleWebKit/537.36 (KHTML, like Gecko) Chrome/80.0.3987.149 Safari/537.36', 'accept-language': 'en,gu;q=0.9,hi;q=0.8', 'accept-encoding': 'gzip, deflate, br'}cookies = dict()def set_cookie(): sess = requests.Session() request = sess.get(url_oc, headers=headers, timeout=5) return dict(request.cookies)async def get_data(url, session): global cookies async with session.get(url, headers=headers, timeout=5, cookies=cookies) as response: if response.status == 401: cookies = set_cookie() async with session.get(url, headers=headers, timeout=5, cookies=cookies) as response: return await response.text() elif response.status == 200: return await response.text() return ""async def fetch_all_data(): async with aiohttp.ClientSession() as session: indices_data = await get_data(url_indices, session) bnf_data = await get_data(url_bnf, session) nf_data = await get_data(url_nf, session) return indices_data, bnf_data, nf_data# Process the fetched datadef process_indices_data(data): global bnf_ul, nf_ul, bnf_nearest, nf_nearest data = json.loads(data) for index in data["data"]: if index["index"] == "NIFTY 50": nf_ul = index["last"] if index["index"] == "NIFTY BANK": bnf_ul = index["last"] bnf_nearest = nearest_strike_bnf(bnf_ul) nf_nearest = nearest_strike_nf(nf_ul)def process_oi_data(data, nearest, step, num): data = json.loads(data) currExpiryDate = data["records"]["expiryDates"][0] oi_data = [] for item in data['records']['data']: if item["expiryDate"] == currExpiryDate: if nearest - step*num <= item["strikePrice"] 0 else strRed(ce_oi) pe_color = strGreen(pe_oi) if pe_change > 0 else strRed(pe_oi) print(f"Strike Price: {strike}, Call OI: {ce_color} ({strBold(f'+{ce_change}') if ce_change > 0 else strBold(ce_change) if ce_change 0 else strBold(pe_change) if pe_change 0 else strRed(ce_oi) pe_color = strGreen(pe_oi) if pe_change > 0 else strRed(pe_oi) print(f"Strike Price: {strike}, Call OI: {ce_color} ({strBold(f'+{ce_change}') if ce_change > 0 else strBold(ce_change) if ce_change 0 else strBold(pe_change) if pe_change < 0 else pe_change})")def calculate_support_resistance(oi_data): highest_oi_ce = max(oi_data, key=lambda x: x[1]) highest_oi_pe = max(oi_data, key=lambda x: x[2]) return highest_oi_ce[0], highest_oi_pe[0]async def update_data(): global cookies prev_nifty_data = prev_bank_nifty_data = None while True: cookies = set_cookie() indices_data, bnf_data, nf_data = await fetch_all_data() process_indices_data(indices_data) nifty_oi_data = process_oi_data(nf_data, nf_nearest, 50, 10) bank_nifty_oi_data = process_oi_data(bnf_data, bnf_nearest, 100, 10) support_nifty, resistance_nifty = calculate_support_resistance(nifty_oi_data) support_bank_nifty, resistance_bank_nifty = calculate_support_resistance(bank_nifty_oi_data) print(strBold(strCyan(f"nMajor Support and Resistance Levels:"))) print(f"Nifty Support: {strYellow(support_nifty)}, Nifty Resistance: {strYellow(resistance_nifty)}") print(f"Bank Nifty Support: {strYellow(support_bank_nifty)}, Bank Nifty Resistance: {strYellow(resistance_bank_nifty)}") print_oi_data(nifty_oi_data, bank_nifty_oi_data, prev_nifty_data, prev_bank_nifty_data) prev_nifty_data = nifty_oi_data prev_bank_nifty_data = bank_nifty_oi_data for i in range(30, 0, -1): print(strBold(strLightGray(f"rFetching data in {i} seconds...")), end="") time.sleep(1) print(strBold(strCyan("nFetching new data... Please wait."))) await asyncio.sleep(1)async def main(): await update_data()asyncio.run(main())

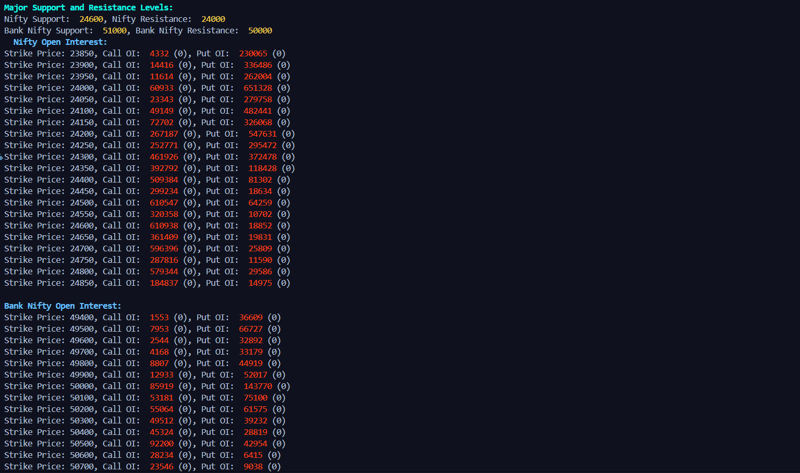

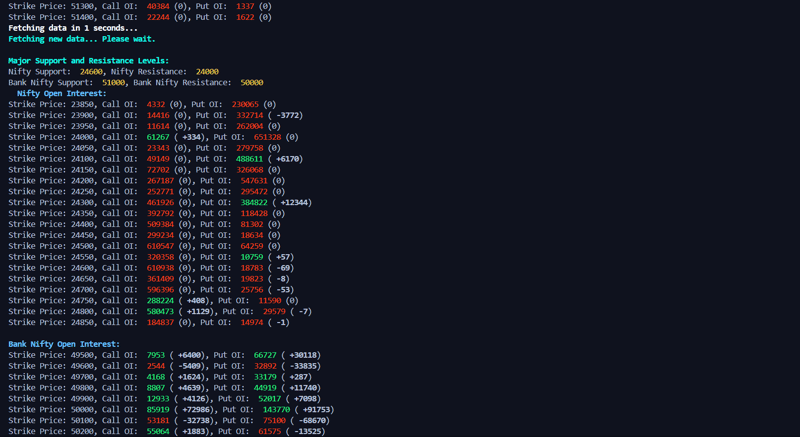

输出:

立即学习“Python免费学习笔记(深入)”;

您甚至可以通过此链接观看演示视频

谢谢!!

我们下一篇富有洞察力的博客见。

以上就是使用 Python 的 NSE 期权链数据 – 第二部分 |沙阿·斯塔万的详细内容,更多请关注创想鸟其它相关文章!

版权声明:本文内容由互联网用户自发贡献,该文观点仅代表作者本人。本站仅提供信息存储空间服务,不拥有所有权,不承担相关法律责任。

如发现本站有涉嫌抄袭侵权/违法违规的内容, 请发送邮件至 chuangxiangniao@163.com 举报,一经查实,本站将立刻删除。

发布者:程序猿,转转请注明出处:https://www.chuangxiangniao.com/p/1348799.html

微信扫一扫

微信扫一扫  支付宝扫一扫

支付宝扫一扫